Review: Recession by Tyler Goodspeed

How a grasshopper caused the 1873 panic, and why recessions are usually just bad luck.

Issue 24 of Works in Progress will arrive with subscribers early next month. Subscribe to receive it, and future issues, straight to your door, workplace, or institution.

What explains recessions? Are they the product of boom-bust cycles? Do they follow cyclical or semi-cyclical patterns? Or are they best viewed by policymakers as being due to surprises changes in the global economy, which economists call ‘shocks’. These are the questions addressed in Tyler Goodspeed’s Recession: The Real Reasons Economies Shrink and What to Do About It.

Economists usually communicate new arguments and data in journal articles. In contrast, Recession is published by Basic Books, an imprint of Hachette, the third-largest publisher in the world. The book is rich with both historical anecdotes and biographical sketches of key players such as Irving Fisher and FA Hayek. Despite this, Goodspeed’s book is a serious, data-rich work.

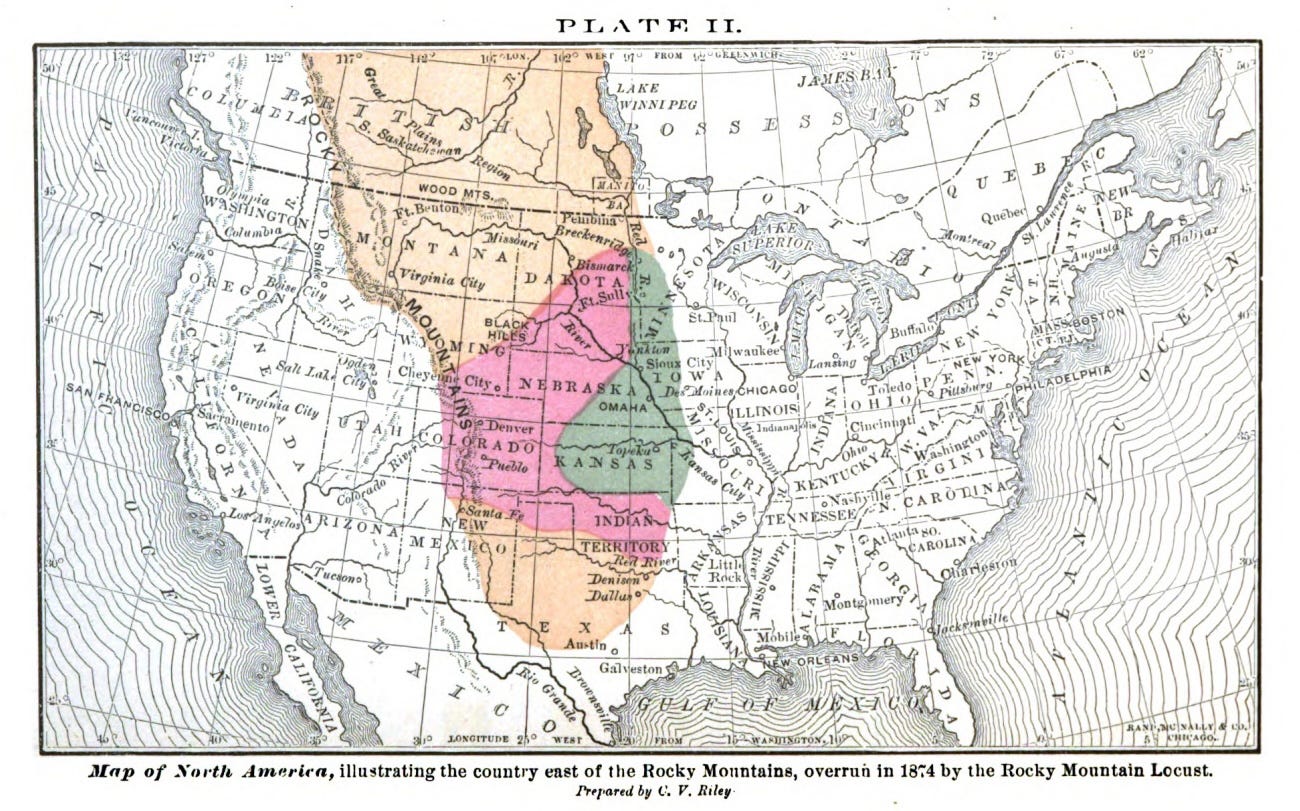

At first glance, Goodspeed’s target is the popular understanding of a boom-and-bust cycle. Consider his vivid account of the crisis of 1873. Both popular and scholarly histories have attributed this recession to railway mania and the collapse of the Northern Pacific Railroad. Goodspeed instead points out the devastating role of a surprise that had nothing to do with economics or economic policy: the great grasshopper plagues of 1873-1876, during which a single locust swarm covered an area larger than California and devastated the very regions the railroad was supposed to open to European settlers.

.jpg){kind=link}

Goodspeed’s first message is that macroeconomic events are not morality plays, nor always under policymaker control or influence. Jay Cooke’s vision of a railway connecting the Pacific northwest was not inherently flawed or hubristic. Nor were other nineteenth-century business busts such as the 1857 New York banking crisis associated with the collapse of Ohio Life. Instead these panics were, like that of 1873, each associated with an idiosyncratic confluence of factors.

The intuitive account of recessions: payback for good times

Goodspeed is not just interested in confronting the kinds of explanations for mania, crashes, and panics seen either in history books or in journalist accounts. He wants to see if the data supports theoretical accounts of recessions that locate the cause of the downturn in the preceding expansion. His antagonists are two celebrated Austrians: first Friedrich Hayek, introduced early in the book as a prospective restaurant dishwasher as a young man in New York and whose prominent account of business cycles rivaled Keynes’s in the 1930s; and second, Joseph Schumpeter, who saw in recessions the opportunity to sort out the mistakes and misallocations of the boom. Goodspeed’s main goal in the 200 or so pages of the book is to ask whether the data supports these theories, or their modern variants, or whether it is consistent with a much simpler story.

The short answer is no, and this is Goodspeed’s second main message. The spine of the book is data on quarterly output for the UK and US. The UK data comes from the work of Steve Broadberry and coauthors. The US data stems from the National Bureau of Economic Research but Goodspeed has extended it back to 1700 and applied a consistent methodology to provide a continuous business cycle series for both countries.

Goodspeed shows that British and American expansions do not resemble Dorian Gray, looking beautiful but hiding an inevitable accumulation of malinvestments (objectively bad investments that are destined to fail) and distorted decisions (mistaken economic decisions taken on the basis of bad regulation or flawed prices) that make a correction inevitable. If they did so, he argues, one would expect that as expansions get longer they get more and more likely to end. In his data, however, the relationship between the age of an expansion and the probability of death is essentially zero. Nor do measures of increased investment during the boom correlate with the severity of a downturn. Nor do longer expansions have longer recessions after them.

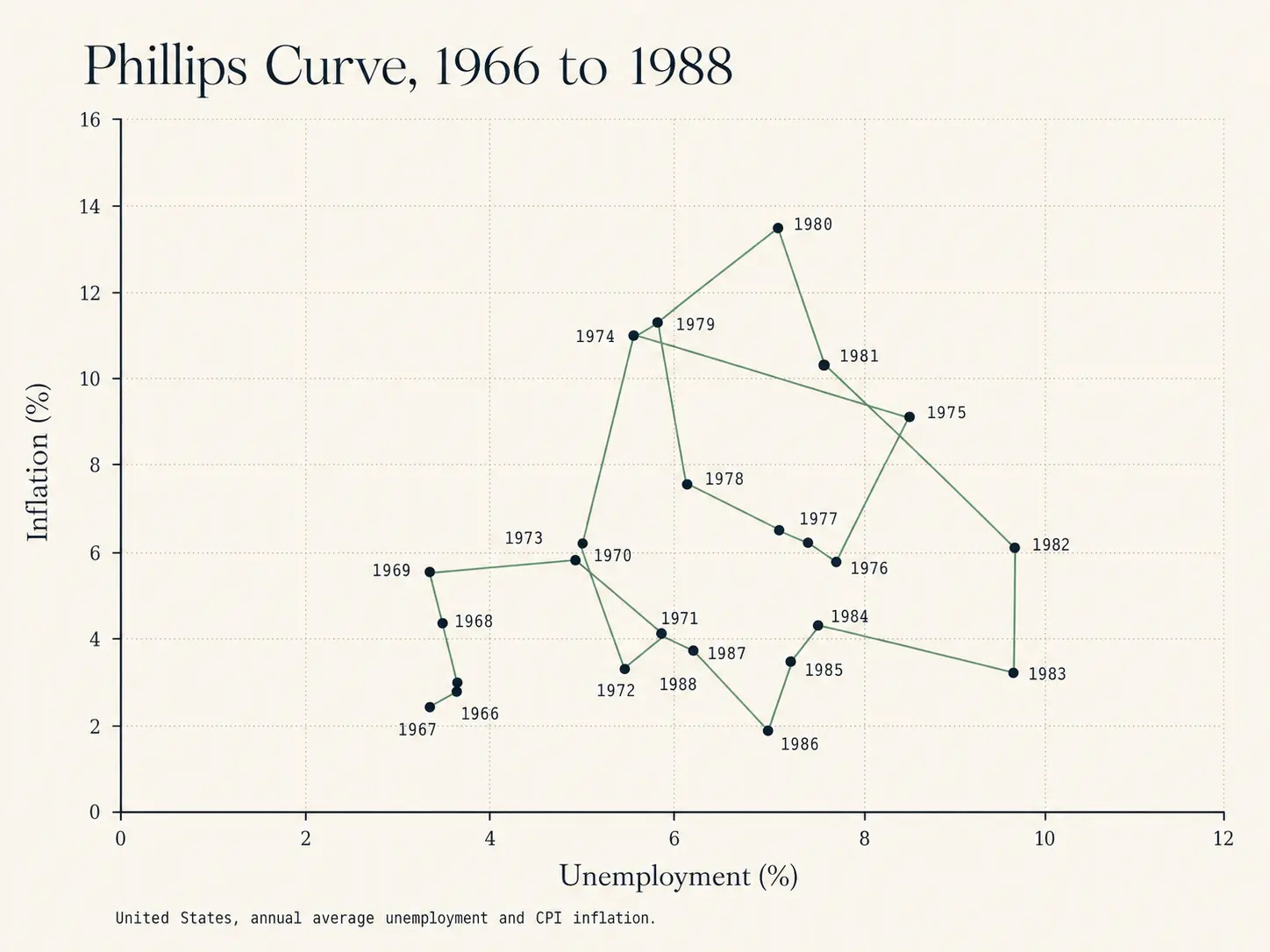

This is why recessions remain essentially unpredictable. Any perceived regularity is likely to be a statistical illusion. Goodspeed shows that attempts to forecast recessions such as inversions of the yield curve (where long-dated government bonds have lower interest rates than short-dated ones) or the Sahm rule (which says a recession is likely underway if the unemployment rate spikes high above its recent lows for three months) are overfitted to US data and don’t work for the UK. The same proved to be true of the Phillips Curve, a strong correlation between unemployment and inflation that existed in British data between 1860 and 1960, which broke down after governments attempted to target it and fine tune the economy in the 1960s.

On top of all this, he finds no evidence that recessions are corrective. Reallocations tend to happen more aggressively during expansions not contractions, contrary to the arguments that Joseph Schumpeter famously made. Similarly, he finds that contrary to common belief recessions tend not to be contagious but rather are mostly patriotic, usually confined to a single country like the modest 2001 downturn in the US (which did not spread to the UK).

Nothing new under the sun

The blurb provided by Niall Ferguson on the hardcover of the book proclaims that it is ‘truly revolutionary’. I would say that Goodspeed’s account is highly consistent with at least one strand of research in macroeconomics.

As Goodspeed makes very clear, his account of recessions has a direct antecedent in Milton Friedman’s so-called plucking model, which is not so much a model as an empirical observation that the path of the economy could just as well be described as a straight trend upwards, which sees negative deviations from the trends and recoveries back to the trend. In Friedman’s view, there is no special reason to see faster-growth periods as artificial booms or bubbles. The goal for policy makers, if Friedman’s model is true, is neither to burst bubbles nor to prevent booms from getting going, but simply to limit or prevent negative shocks and ameliorate their consequences.

Goodspeed’s historical case studies are also consistent with a much derided tradition in macroeconomics, known as real business-cycle theory, associated with economist Ed Prescott, who won the Nobel Prize in 2004 and died in 2022. In real business-cycle theory, the economy ticks along its regular path until it is hit by what real business-cycle theorists call ‘technology shocks’. Former US Treasury Secretary and Harvard President Larry Summers objected to these models because technology shocks were undefined. Goodspeed’s narrative accounts provide compelling examples of how shocks broadly understood can account for much business cycle behavior.

I recall being distinctly unimpressed by this emphasis on shocks as an undergraduate. Nonetheless, it is clear that until recent times, most economic fluctuations were caused by exogenous factors such as the climate. What Goodspeed emphasizes is that exogenous shocks have played an important role even into modern times.

For example, recent research has demonstrated the role of bank failures in explaining the depth of the Great Depression. Goodspeed notes that huge locust plagues like those of 1873 ravaged western and central states. By late 1931, one in six farms in this region was underwater. So while contemporaries blamed land speculation and irrational land booms, it is clear that exogenous shocks to the real economy lay behind part of the severe banking distress of the early 1930s. Again, Goodspeed notes that this wasn’t The Cause of the Great Depression. There was no one cause, ‘but rather a succession of overlapping and interacting shocks, often highly region-specific’.

Predicting such events is a fool’s errand. Rather, Goodspeed argues we should imagine several dice being rolled as if in a game of chance. A roll of one is a negative shock: a war or a coal-strike or a climatic shock. A recession might occur if we simultaneously roll three ones.

If you’re in a hole, stop digging

Not all shocks are necessarily exogenous in nature. Chapter 7, entitled ‘Firefighters and Arsonists’, notes that while policymakers can play a vital role in smoothing shocks and responding to a crisis, they have often themselves acted as arsonists.

The actions of the Federal Reserve during the Great Depression are a famous example. Wary of speculative finance, the Fed allowed the money supply to fall precipitously and failed to halt the banking collapse. The shock here was hardly exogenous to the economy itself but the type of unforced error that is sadly not unusual in the historical record.

Similarly, conventional accounts at the time of the Great Recession of 2008 emphasized financial malfeasance in the housing market with subprime mortgages being repackaged to unsuspecting lenders. But why should these issues in the banking sector produce a worldwide recession? Moralizing accounts that emphasize the greed of bankers can be politically and emotionally satisfying but they don’t explain the scale of the downturn. The vast majority of the homes built during the bubble between 2002-2006 turned out to be entirely consistent with subsequent demand.

Goodspeed sees the 2008 recession as caused by a confluence of largely independent and to a degree avoidable shocks. There was a negative supply shock that saw the price of gasoline reach $5.86 per gallon in 2026 prices (at time of writing still an all-time real terms high). As a result, fertilizer prices also spiked. This energy-shock-induced slowdown began before distress in financial markets resulted in the collapse of Lehman Brothers. But this shock itself would not be nearly enough to explain what then happened.

Rather, as monetary economists such as Robert Hetzel and Scott Sumner have argued, monetary authorities then responded to this shock to prices by tightening policy at precisely the wrong time. In Spring and Summer 2008, the Fed failed to decisively lower interest rates in the face of declining economic activity. Goodspeed highlights the particular errors made by Alistair Darling in failing to agree to a US proposal to bail out Lehmans on the grounds that this would be importing the US contagion. Regardless of the rights or wrongs of that particular decision, Goodspeed’s account is consistent with those who see the crisis of 2008 as at least partly caused by a departure from the standard monetary policy procedures during the Great Moderation.

Prepared to get schooled in my Austrian perspective

It is worth asking how adherents of either FA Hayek’s Austrian business cycle theory, which says, effectively, that the bust is punishment for an unsustainable boom, or Hyman Minsky’s financial instability hypothesis, which says that highly financialized economies are inherently unstable, would react to his arguments.

The Austrians might challenge whether Goodspeed’s empirical tests map onto the theoretical objects they are meant to be testing. For example, Goodspeed’s data show that longer expansions don’t predict deeper or longer recessions. But the Austrian claim is subtler: it is comfortable with a short expansion generating more malinvestment than a long, sound-money expansion, if the short expansion is driven by massive credit inflation. The Austrian story is fundamentally microeconomic: it predicts distortions in specific investment decisions and the accumulation of these decisions across the economy produces macro-level effects. This is hard to test with Goodspeed’s data and without firm-level data on investment and capital decisions, it seems like the two views risk talking past each other.

The Minskyites would say that Goodspeed had proven them right. Goodspeed acknowledges that recoveries from a financial crisis or credit crunch tend to be slower. But it isn’t apparent from his framework or Friedman’s plucking model why this should be the case. If financial recessions are qualitatively different from other types of recession, this suggests that the state of the financial system at the time of the shock matters, meaning that Minsky’s concerns about financial fragility cannot be dismissed.

The data that Goodspeed has assembled is impressive but it covers just two countries. The experience of a broad set of countries might reveal still more of a role for financial overextension or capital market distortions. These responses notwithstanding, Goodspeed does pose important challenges for adherents of either Hayek or Minsky. If the empirical data Goodspeed offers is not an adequate test, then it becomes incumbent on them to at least propose tests which would offer a fair hearing for their theories. If they cannot do that, their theories risk becoming more metaphysics than economics.

An end to boom and bust?

So, does Goodspeed’s book succeed in smiting the myth of the boom-bust cycle? Without doubt, he lays to rest many suppositions or beliefs many have about business cycles. The book is a great read and packs a lot of analysis into its 200 pages. The datawork of the book is itself an important contribution. While I don’t see Recession as the final word on this topic, readers will update their priors about the extent to which shocks to the economy such as the 2026 US-Iran conflict have been the key drivers of many economic downturns. In contrast, plausible and intuitive accounts that both non-specialists and specialists alike have offered for an endogenous business cycle, where booms sow the seeds of eventual busts, struggle to find support in his data.

Personally, Recession strengthened my prior beliefs that policymakers simply don’t have enough information to even distinguish between a robust expansion and a speculative bubble in real time, let alone the tools to safely tame any bubbles that they did find. Rule-based monetary policy, which allows market participants to form stable expectations about what its response will be, while still allowing flexibility in the event of shocks, might be the best we can hope for. Here Goodspeed’s advice is sensible: policymakers should first do no harm before thinking that they have the ability to entirely tame the business cycle.

Mark Koyama is professor of political economy at the Hamilton School, University of Florida.

| A guest post by

|

The Schumpeter finding is the most consequential one here. If longer expansions don't produce more severe recessions — if the creative destruction mechanism doesn't actually clean up the misallocations from the boom — then the self-correcting assumption that underlies a lot of structural economic policy loses its empirical foundation. The implication worth drawing out is that structural problems don't resolve themselves through the cycle. They persist. Which means the gap between what an economy produces and what typical workers receive isn't a temporary distortion that the next recession will correct — it's a design condition that requires active structural intervention rather than cyclical patience. Goodspeed's data undermines the 'wait for the correction' argument more thoroughly than most readers will notice on first pass.

Last paragraph.

This century monthly PMI were a godsend for spotting issues quite reliably and early allowing interest rates to be lowered and recessions mitigated or averted.

While a good thing i cant help but feel that the longer a boom the harsher the recession.

On a side note oil price spikes with their knock on to inflation and interest rates have seemed to be the harbinger of most recessions I have witnessed in a blessedly long life.