How New Zealand invented inflation targeting

The political gamble that made modern central banking

This is an article from the new issue of Works in Progress, Issue 19. Read the full issue, including pieces on the end of lead in the developing world and brain-computer interfaces, on our website.

Oscar Sykes explains how one Kiwi tamed inflation.

Most central banks today target inflation: the government announces a numeric target for inflation that the central bank is tasked with achieving by changing interest rates, setting reserve requirements, and buying and selling financial securities. They haven’t always. Before the 1990s, many targeted the money supply or an exchange rate.

This change did not come from research by economists or the emergence of an expert consensus that central banks should reform. Instead, New Zealand's Finance Minister in the 1980s, Roger Douglas, started it when he publicly announced explicit inflation goals to demonstrate his commitment to price stability. This political decision would lead to New Zealand's central bank formalizing a system of inflation targeting.

When it was announced, inflation targeting drew skepticism from policymakers and economists. It nonetheless proved very successful. What started as a small nation's attempt to tame inflation would go on to become standard practice among central banks globally. Only since then – after its implementation worldwide – has an extensive academic literature built up explaining how and why the system works.

Credit card financing

Historically, New Zealand ranked among the world's wealthiest nations. An enormous ratio of farmland to people, along with privileged trade relations with Britain, powered a strong agricultural export economy.

However, during the mid-20th century its economic position was deteriorating. In the 1970s New Zealand progressively lost its preferential market access to the UK after Britain joined the European Economic Community. The country was also hit hard by the global oil crises of 1973 and 1979. In the two decades between 1960 and 1980 New Zealand's income per head fell from 3rd to 17th among 24 OECD countries.

The government controlled large portions of many industries, including banking, insurance, and utilities, and the agricultural sector was supported by generous subsidies, price guarantees, and low-interest loans. Imports of goods were also tightly controlled – Kiwis needed government approval to subscribe to an overseas magazine.

High inflation was a problem throughout this period, peaking at 17.2 percent in 1980. This was partly caused by the dual oil crises which pushed up energy prices around the world, but was made worse by large budget deficits and inflationary monetary policy.

Unlike today's central banks, which mainly control inflation through adjusting interest rates, New Zealand used direct regulatory controls on financial institutions. The government forced banks to hold specific amounts of government debt and set limits on interest rates for savers. It used capital controls to restrict money flows in and out of the country, allowing it to retain a fixed exchange rate.

New Zealand’s central bank, the Reserve Bank, operated under direct government control with political interests heavily influencing monetary policy. Anti-inflation measures, such as those implemented in 1976 and 1977, were abandoned once their economic costs were felt. Leading up to the 1981 election, Prime Minister and Finance Minister Robert Muldoon ignored his advisers' repeated calls for tighter monetary policy, which is when authorities restrict the flow of money through the economy. Inflation began to fall in 1982, but only after Muldoon imposed a complete freeze on prices and wages, which then coincided with an economic contraction.

In June 1984, a visibly drunk Muldoon shocked the nation by announcing a snap election on live TV, scheduled for a month's time. When a reporter remarked, 'That doesn't give you much time to run up to an election, Prime Minister', Muldoon retorted, 'Doesn't give my opponents much time to run up to an election, does it?’

After the opposition Labour Party won the election decisively, the departing Prime Minister left an ominous message for his successor, David Lange, warning him that bad news was waiting: for the past month, New Zealand had been experiencing a run on its dollar, which was widely considered overvalued. The snap election triggered a major selloff. In the first hour of trading following the announcement, the Reserve Bank sold more foreign currency than it normally would in an entire month.

Despite Bank officials advising Muldoon three times to devalue the currency to curb the selling, he refused. To defend the exchange rate, the Reserve Bank and Treasury borrowed NZ$1.7 billion to keep buying New Zealand dollars, straining public finances. Lange later said, ‘We actually were reduced to asking our diplomatic posts abroad how much money they could draw down on their credit cards!’

Rogernomics

Upon taking office, the Labour government launched an ambitious series of free market reforms, which became known as Rogernomics, after the Minister of Finance, Roger Douglas.

The government devalued and then floated the currency. It lifted the wage freeze. Many state-run organizations laid off staff. The railways reduced its workforce from 21,000 employees to 5,000. The top income tax rate was halved from 66 to 33 percent. Industry subsidies were cut significantly, falling from 16.2 percent of government spending when Labour took office to 4 percent by 1994.

The speed and expansiveness of the reforms were extraordinary. David Henderson, OECD's then-Chief Economist, called the reforms 'one of the most notable episodes of liberalization that history has to offer'.

However, these changes temporarily worsened inflation, rising from 6.2 to 15.4 percent between 1984 and 1985. Removing the wage freeze released pent-up inflationary pressure, while the currency devaluation led to a large inflow of overseas capital.

The new government was committed to getting inflation down. Recent experiences overseas showed countries could successfully rein in high inflation using tight monetary policy. Paul Volcker’s Federal Reserve dropped inflation from 13.5 percent in 1980 to 3.2 percent in 1983 by raising rates to nearly 20 percent. Future Reserve Bank Governor Don Brash, said, ‘[controlling inflation] was not an impossibility: it could be done; Paul Volcker had proved it’.

This shift was also influenced by the growing consensus among economists that in the long-run monetary policy can only meaningfully affect prices, and not real activity like output and employment. Previously, many economists believed that inflation had a reliable inverse relationship with both unemployment and economic output, as described by the Phillips curve (named after Kiwi economist Bill Phillips). This theory suggested that accepting higher inflation could lead to persistently lower unemployment.

Throughout the 1970s, nations like the US and UK had experienced significant inflation alongside rising unemployment, a phenomenon termed stagflation. This broke the apparent relationship between higher inflation and employment, and led an increasing number of economists to believe that persistent high inflation had no benefits.

Roger Douglas and his advisers shared this view. As part of their reforms, they granted the Bank de facto independence, giving it autonomy to make day-to-day decisions without political interference. They also instructed the Bank to prioritize reducing inflation, over its other statutory objectives to promote production, trade and employment.

They moved from direct controls, which required ministerial sign off, to conducting monetary policy indirectly through adjusting banking system liquidity, essentially changing how much money there was for banks to borrow.

Inflation seemed high during this period, reaching 15.7 percent by 1987, but this was largely due to the introduction of a 10 percent VAT in 1986, which made prices surge. Removing this effect, inflation was on a steady decline.

A lack of alternatives

Following these encouraging signs, Douglas invited the Reserve Bank board to consider further changes to better control inflation.

The objective was to find a framework for making monetary policy decisions that would make them more consistent and credible, which would increase their effectiveness. One such approach was monetary targeting, where central banks aim to grow the money supply at a pre-announced rate. Over the previous two decades, many major economies, including the US, UK, and West Germany, had adopted it. The logic was straightforward: economists had observed a strong historic relationship between the amount of circulating money and inflation. If too much money chased too few goods, prices would rise. By controlling money supply growth, central banks believed they could control inflation.

The decision to focus on intermediate targets like the money supply, rather than direct goals like inflation, was practical. These targets were more directly under central bank control and appeared to respond more quickly to policy changes, making it easier to judge effectiveness.

While monetary targeting seemed compelling in theory, central banks often missed their targets or found that meeting them didn't control inflation as intended. Financial innovations and deregulation during this period made the money supply more volatile and harder to control.

These challenges led many countries to abandon or de-emphasize monetary targets. But despite the dissatisfaction, there was a lack of compelling alternatives. A Reserve Bank of Australia paper noted: 'The difficulties in using monetary aggregates are well-known [...] The nagging question is, with what is such an objective to be replaced?'

Having seen this experience overseas alongside huge fluctuations in the money supply following New Zealand’s financial liberalization, there was little appetite among officials for monetary targeting.

While these discussions were happening, Douglas was becoming worried that inflation might be starting to plateau. Although inflation had fallen substantially from its peak by 1988, inflation expectations among businesses over the next two years were still at 6.7 percent.

In March 1988, he spoke to his advisers about the need to convey the government's commitment to further disinflation. They left the meeting unsure how seriously to take these remarks.

This left them surprised when, the very next day, Douglas appeared on TV declaring his intention to reduce inflation to 'around 0 or 0 to 1 percent' over the next couple of years, and then went on to make several similar comments in the following days.

Douglas would soften his stance on specific timelines but ask the Reserve Bank and Treasury to develop public inflation goals for the next few years that would support his earlier statements. The Bank added 1 percentage point to Douglas's upper range to account for the measurement bias in inflation data at that time, arriving at a target range of 0–2 percent. Michael Reddell, head of the Reserve Bank’s monetary policy unit, said it was settled on ‘more by osmosis than by ministerial sign-off’.

This development led officials to entertain the idea of making inflation targets part of the Bank’s monetary policy framework. David J. Archer, a former Assistant Governor, said inflation targets were eventually chosen ‘as the least bad of the alternatives available'.

This raised several tricky design questions. The original inflation reduction target announced by Douglas was intended as a communication tactic to shift expectations. As this was a time-defined target set by the government, there was room to assess results based on market conditions. A statutory framework governing the central bank would offer far less flexibility.

Large shocks to the economy could put the Bank in a position where meeting its target would be infeasible or undesirable. It wasn't clear how to design targets that would signal intentions effectively while maintaining necessary flexibility. For the initial targets, the Bank reluctantly agreed shocks would be dealt with by renegotiating the target with the Finance Minister.

The Bank was also concerned that inflation targets provided less basis for evaluating performance compared to intermediate measures, saying it required the public to adopt a 'trust us, we know what we are doing' attitude. Officials believed strong transparency was needed to provide insight into the Bank's decisions. This would help with accountability and legitimize authority granted to unelected policymakers.

This led to the introduction of Monetary Policy Statements, which are reports Governors must publish biannually, reviewing past policy decisions and outlining future intentions. These statements are then scrutinized by Parliament.

In parallel with this, there was a separate stream of work focused on how to enshrine greater central bank autonomy through legislation. Douglas wanted to reduce the risk that future governments would revert back to using monetary policy for political purposes.

The Reserve Bank's view was shaped by work on time inconsistency, which identified a fundamental problem: even when policymakers announce the best possible plan, they often face incentives to deviate once people have acted on the announcement. As rational people can anticipate this temptation to change course, they won't believe the original policy statement.

Following this logic, the Reserve Bank advocated for a model in which price stability would be mandated by law and implemented by the Bank's Board. But the Treasury stressed the need for political oversight of central bank officials to keep them accountable.

What emerged was a novel compromise. Unlike the Federal Reserve or the Bundesbank, which enjoyed broad independence, the Reserve Bank was granted operational independence only, the freedom to use monetary policy instruments to achieve agreed goals, but not to set those goals themselves. The Bank was also given a singular focus: price stability, removing previous objectives around employment, output, and trade.

This was combined with a single decision-maker model to establish accountability. The Bank's governor was granted sole authority and held accountable for their actions. Upon appointment, each new governor negotiated targets with the Finance Minister and could be dismissed for failing to meet them. While the government retained the right to override the Reserve Bank's objectives for up to a year, this had to be done publicly through a parliamentary order. The aim was to allow government intervention during crises while discouraging politically motivated interference due to its public visibility.

Success

A new Reserve Bank Act was passed in December 1989 and came into effect in February 1990. Governor Don Brash was tasked with reaching the 0–2 percent target by the end of 1992. To the great surprise of many, it was achieved a year ahead of schedule in December 1991.

Brash did this by maintaining tight monetary policy, which led unemployment to rise sharply. From Brash’s appointment in 1988 to the achievement of the target three years later, unemployment increased from 6.4 to 11 percent. (Although the 1987 global stock market crash and wider reforms likely also played a part.)

Over the next twenty years the framework delivered on its promise. New Zealand experienced the kind of price stability that would have been unthinkable during the chaotic 1970s and 80s.

The Act has been successful in preventing the use of monetary policy for political benefit – the override provision has never been used (though its use has been considered).

Reforms did introduce greater flexibility: the system of renegotiating targets when shocks occurred was quickly determined to be impractical, and frequent renegotiations risked undermining the credibility of the targets. The policy was quickly refined. A revised set of targets was signed in December 1990, outlining situations where the Governor would be allowed to deviate from their target. In these situations they would be assessed on their judgement in responding to the economic disruption. Later changes increased this freedom, stipulating that the targets should be achieved on average over the medium-term, rather than having to be met constantly.

A new consensus

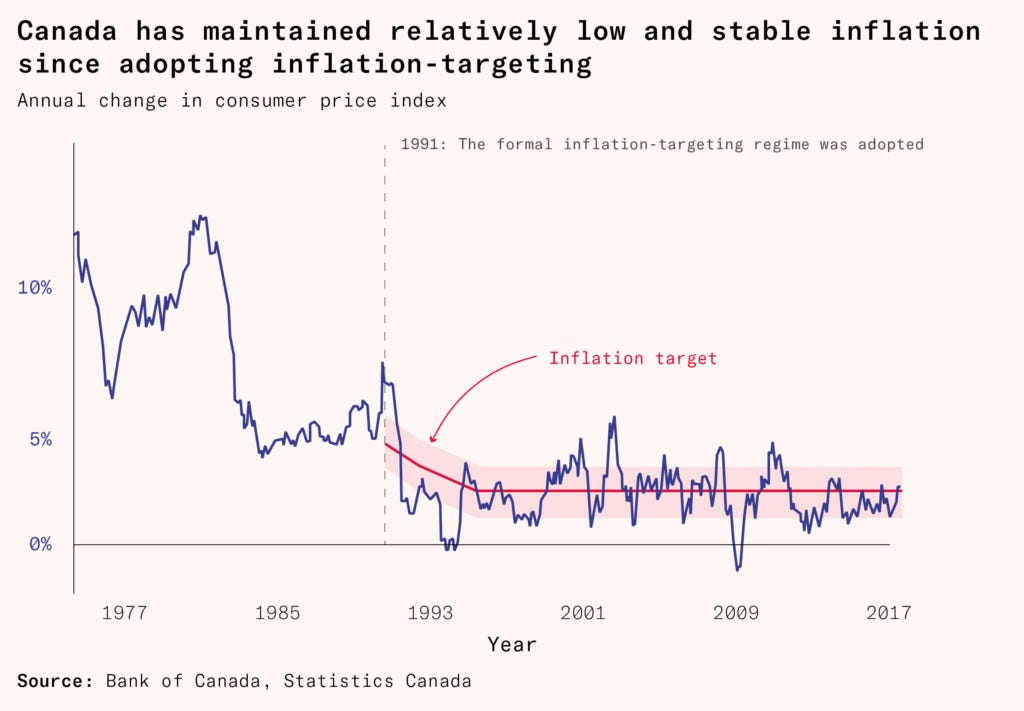

After New Zealand, it started to spread globally. Canada was the next country to adopt inflation targeting. From 1975 to 1982, Canada followed monetary targeting. Like other nations, it had a disappointing experience. Despite largely meeting its money supply goals, inflation remained persistently high, averaging 8 percent over the period. This led it to drop the target. Then-Governor Gerald Bouey said, 'We didn’t abandon monetary aggregates, they abandoned us'.

The country’s Finance Minister, Michael Wilson, directed Governor John Crow to develop inflation reduction targets. These were unveiled in February 1991 through a joint announcement between the government and Bank of Canada. The plan established time-based targets to reduce inflation from 6.2 percent to between 1 and 3 percent by 1995. In March 1991, Canada’s Crow met with fellow central bankers in Basel at the Bank for International Settlements. His shift to inflation targeting faced significant criticism. Former Deputy Governor John Murray characterized the prevailing sentiment: 'Why would any prudent central bank risk its reputation by accepting such an uncertain and explicit mandate? The chances of [meeting the targets] were regarded as extremely small and would likely undermine the Bank's credibility'. These concerns weren't unfounded, simulations of forecasted inflation showed the 65 percent confidence interval extending well beyond the target range.

However, due to raising rates combined with a timely economic downturn that was already cooling the economy, inflation fell to 1.5 percent by 1992. Much like New Zealand, in subsequent decades, Canada maintained relatively low and stable inflation. From inception until 2018, Canada's average inflation rate was 1.9 percent, remarkably close to its 2 percent target midpoint.

Between 1992 and 1993, the United Kingdom, Sweden, Australia, and Finland all adopted inflation targeting. Notably, all except Australia did so soon after their fixed rates collapsed within the European Exchange Rate Mechanism.

It isn't clear how exclusively New Zealand was responsible for this sudden adoption. Crow said the proximate cause of Canada’s targets was the directive he received from the Finance Minister, but the Bank of Canada would consult Reserve Bank staff on New Zealand's experience. Lord Mervyn King, then the Chief Economist of the Bank of England (and later its Governor), said, ‘The idea of an inflation target was certainly influenced by conversations with the Reserve Bank of New Zealand staff. The details of implementation were home grown’.

In the 1990s, eleven EU member states formed the European Monetary Union as a prelude to the common adoption of the euro currency, with the European Central Bank adopting a framework resembling inflation targeting (despite not labelling itself as such).

The IMF and several academic economists initially argued that, despite encouraging signs in advanced economies, inflation targeting may not be appropriate for developing countries. A 1998 IMF paper outlined preconditions deemed necessary for successful adoption including substantial central bank independence, technical capacity to forecast inflation, and well-developed financial markets. Since these were largely absent in developing economies, the IMF considered the regime unsuitable and recommended alternatives such as pegged exchange rates.

However, the IMF later revised its position after successful implementations in countries like Chile (1999) and Mexico (2001). A 2006 paper by two IMF economists concluded: 'The survey evidence indicates that it is unnecessary for countries to meet a stringent set of institutional, technical, and economic "preconditions" for the successful adoption of inflation targeting'.

Today, almost all developed countries and many developing nations target inflation.

Why did inflation targeting become so widely adopted? One obvious reason is that it solved the practical problem of the money supply and other intermediate targets being imperfect proxies for what governments actually care about.

Fears about central banks losing credibility by failing to meet their targets mostly didn't materialize. The introduction of inflation targeting coincided with a period known as the great moderation where there was unusually low inflation and economic volatility. There is some debate about how much inflation targeting was responsible for it, but it did mean central banks were largely able to set and meet low inflation targets.

Inflation targeting appears to have stabilized public inflation expectations significantly. A Dallas Federal Reserve paper found that countries adopting inflation targeting experienced much smaller increases in inflation expectations following inflation spikes. This was true when compared both with their pre-targeting period and with non-targeting countries. When people believe the central bank will maintain its target, they factor this into wage and price-setting decisions. This reduces the need for large interest rate hikes that might cause economic downturns and job losses when fighting inflation.

It has also meant concerns that inflation targeting would lead to harmful outcomes during shocks haven't been a big issue. The credibility gained through stabilised expectations has allowed banks to act more freely while maintaining market confidence in their commitment to control inflation. This can be seen in the shift towards focusing on achieving targets over the medium-term and getting more flexibility to deviate from their targets under certain conditions.

Inflation targeting also tends to encourage other institutional improvements. These include central bank independence, as this helps central banks achieve their mandate, and transparent communication, as this makes governments more comfortable delegating monetary authority.

These features help reduce the political interference and short-termism of earlier systems, as demonstrated in pre-reform New Zealand where anti-inflation measures were abandoned for political convenience. By aligning incentives and providing transparency, they create accountability without allowing political pressures to distort economic decision-making.

New Zealand’s monetary reforms were marked by disagreement, improvisation, and unexpected turns. As Don Brash later said:

Perhaps there were some advantages to being a late starter [...] Against this background the idea began to form that it might be better to target inflation directly. The transition, however, was not well-defined [...] I will simply note that history can be surprisingly confusing, even for those who were there.

Inflation targeting didn't emerge from academic research. Roger Douglas wanted to show his commitment to price stability, and inflation targeting offered a way to do it. While economists were crucial in translating this political initiative into a workable institutional framework, it was Douglas who put the idea on the table. After New Zealand and Canada demonstrated inflation targeting's effectiveness, other countries quickly followed suit. Delivering the results is what caused consensus to shift.

Oscar Sykes is a software engineer. You can follow him on Twitter here.

Great article! I learned a lot.

Pure inflation targeting (without employment, or other strategic factors) seems to privilege the financial class above all others; and RbNZ ‘independence’ has seen us accrue - two hundred billion dollar deficit in public infrastructure. “The wealth of nations”. So, a mixed bag at best ?